So, you’ve reviewed your spending and created a budget, and now you know exactly how much you spend on your home, your car, discretionary spending, and how much you divert to your retirement accounts. That’s great and all, but what about other savings, such as for an emergency? Do you know how to easily separate all your expenses with the amount of income you’re bringing in?

Harvard bankruptcy expert Elizabeth Warren coined the “50/30/20 rule” for spending and saving money back in 2005. Thousands of people around the world now use this rule of thumb for organizing their budgets each month. Read more to learn how to implement this budgeting rule in your own life.

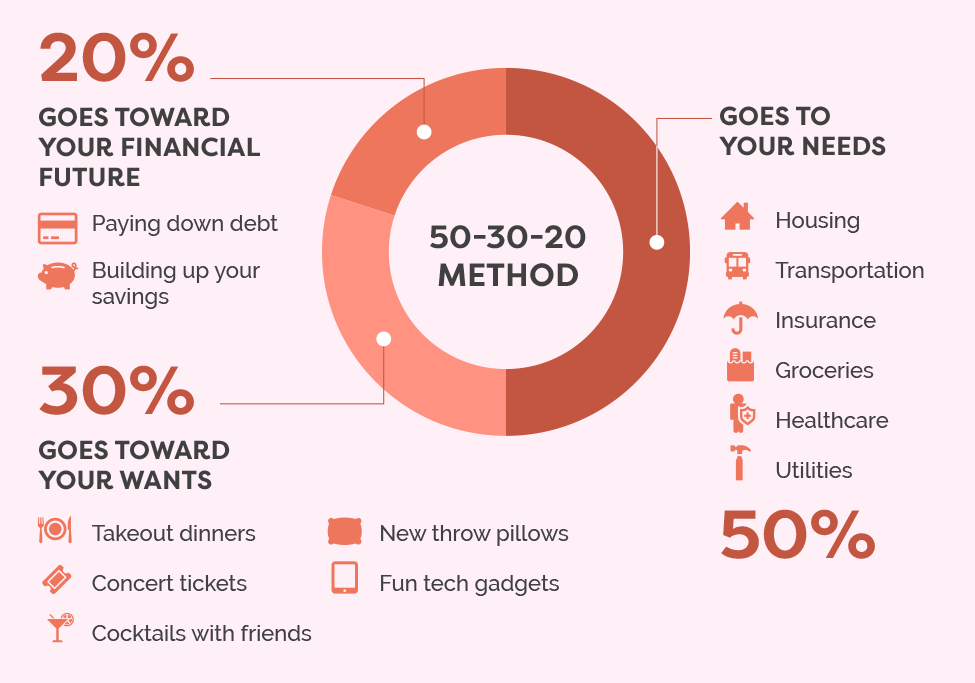

What is The 50/30/20 Rule?

The 50/30/20 rule helps you build a budget by using three spending categories

50% of your income should go to living expenses and essentials. This includes your rent, utilities, and things like groceries and transportation for work.

20% of your income should go to financial goals, meaning your savings, investments, and debt-reduction payments (if you have debt, such as credit card payments).

30% of your income should be used for flexible spending. This is everything you buy that you want but don’t necessarily need (like money spent on movies and travel).

Keep in mind that the percentages for essentials and flexible spending are the maximum you should spend. Falling under those guidelines can leave you with more money for other financial goals.

1. Calculate Your Income After Tax

The 50/30/20 rule does require a little homework before you begin. Your after-tax income is what remains of your paycheck after taxes are taken out, such as state tax, local tax, income tax, Medicare, and Social Security. If you have a steady paycheck, this should be easy to figure out. Look at your pay stubs. If health care, retirement contributions, or any other deductions are taken out of your paycheck, add them back in.

If you’re self-employed, your after-tax income equals your gross income less your business expenses, such as the cost of your laptop or airfare to conferences, as well as the amount you set aside for taxes.

2. Limit Your “Needs” To 50% Of Your After-Tax Income

![]()

Go back to your budget and figure out how much you spend on “needs” each month. These are things like groceries, rent, utilities, health insurance, car payments, etc. According to the 50/30/20 rule, the amount that you spend on these things should total no more than 50 percent of your after-tax pay.

Make sure you properly differentiate between which expenses are “needs” and which are “wants.” Basically, any payment that you can forgo with only minor inconveniences such as your cable bill or back-to-school clothing is a want. Any payment that would severely impact your quality of life, such as electricity and prescription medicines, is a need.

3. Limit Your “Wants” To 30%

I know this sounds pretty good. 30% of your money going to what you want. Hello there gorgeous shoes, resort vacations, salon-quality haircuts, and fancy restaurants. Wow, the 50/30/20 rule makes it easy to get all the beautiful things I’ve ever wanted!

Not exactly. Remember how strict we were with the definition of a “need”? Your “wants” don’t include extravagances. These include the basic niceties of life that you enjoy, like that unlimited text messaging plan, your home’s cable bill, and cosmetic (not mechanical) repairs to your car.

You might be spending more on “wants” than you think. Yes, the rules are tricky, but if you think about it, they do make sense.

4. Spend 20% On Savings & Debt Repayments

This last step in the 50/30/20 rule is most important for long-term. You should spend at least 20 percent of your after-tax income repaying debts and saving money in your emergency fund and your retirement accounts. If you’ve got a credit card balance you carry, the minimum payment is a “need” and counts toward the 50%. Anything extra is an additional debt repayment, which goes toward this 20% category. If you carry a mortgage or a car loan, the minimum payment is a “need” and any extra payments count toward savings and debt repayment.

Why Does The 50/30/20 Rule of Thumb Work?

The 50/30/20 rule keeps your personal finances simple and stable so you can pay your bills, add to your savings, and have the freedom to use some money just for fun. It’s also a perfect starting point for a budgeting novice. There’s no uncertainty, your action steps are clear, and it even provides for savings, investments, and other financial goals. This makes it much more likely that you’ll stay the course over time, ultimately reaching your desired financial stability.

Many people use the 50/30/20 rule is used by so many people because it offers some flexibility. It’s not against the rules to bend the percentages a little to better fit your life. It’s not about the exact percentage breakdown since all budgets are slightly different. The key is to find a financial system that keeps you consistent in managing your money every month. You’ll be better prepared to make payments, more responsible with your savings, and still, have room to be able to enjoy life!

Want More Personal Finance Tips? Click Here: Nxt Modern Money